This week, we published a new report looking at the world of Corporate Venture Capital funds accessible here.

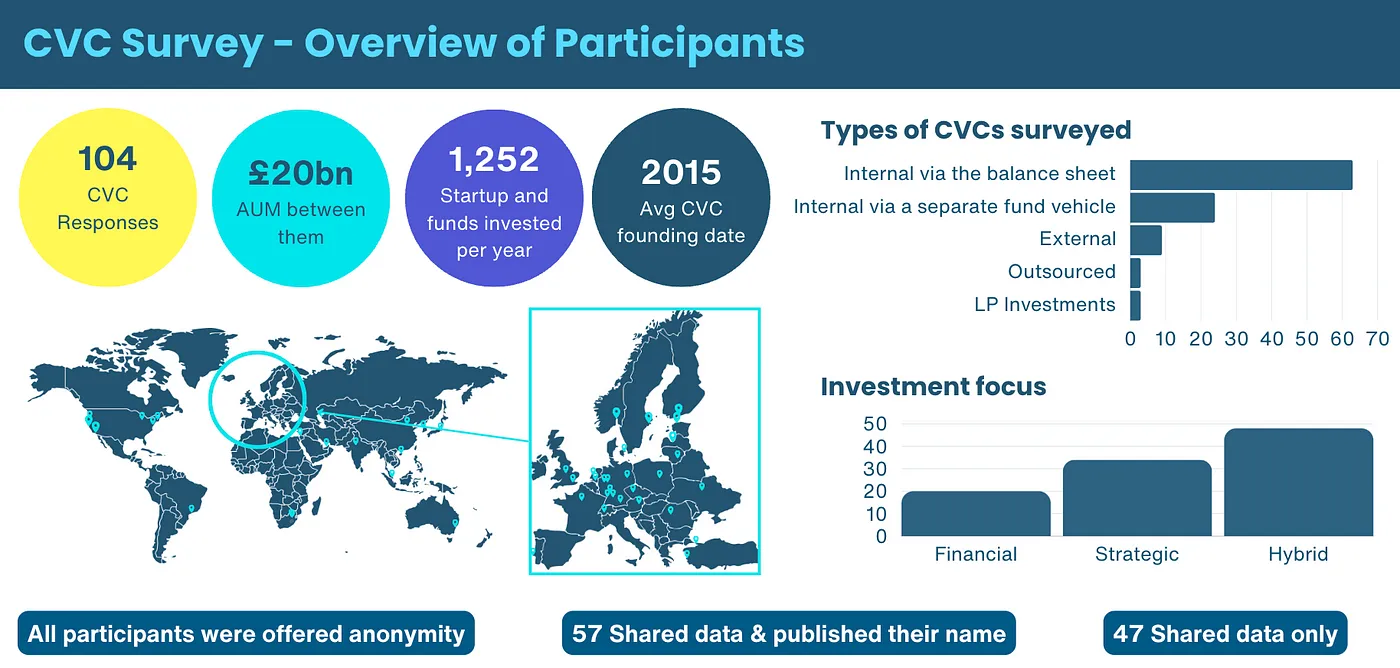

The report provides insights from 100+ global CVC investors with over £20 billion in assets under management deployed into over 600 startups and VCs per year. It’s the first time such a comprehensive analysis has been conducted with a focus on venture in corporate venturing. The resulting study outlines the theses, investment processes and insights from one the fastest-growing investor bases of the last decade.

As well as summarising the key insights from the survey, we cover qualitative factors such as the benefits and disadvantages for founders of raising from a CVC, and the challenges for corporates of setting up a corporate investment vehicle.

It’s published in partnership with Mountside Ventures, and with support from Sheridans, Dealroom and FieldHouse.

Context

1 in 4 deals now include a CVC, yet there continues to be very little information for founders on this asset class. Although no two CVCs are the same, we have tried to separate them by type and structure, to provide practical advice.

By combining results from surveying over 100 CVCs actively investing in founders and funds, as well as analysing data on CVC investments over the last 15 years in Europe, we hope to provide a guide to the tech community and share best practices through case studies and the do’s and don’ts of corporate investing.

Summary of Findings

We’ve summarised the conclusion of the report below:

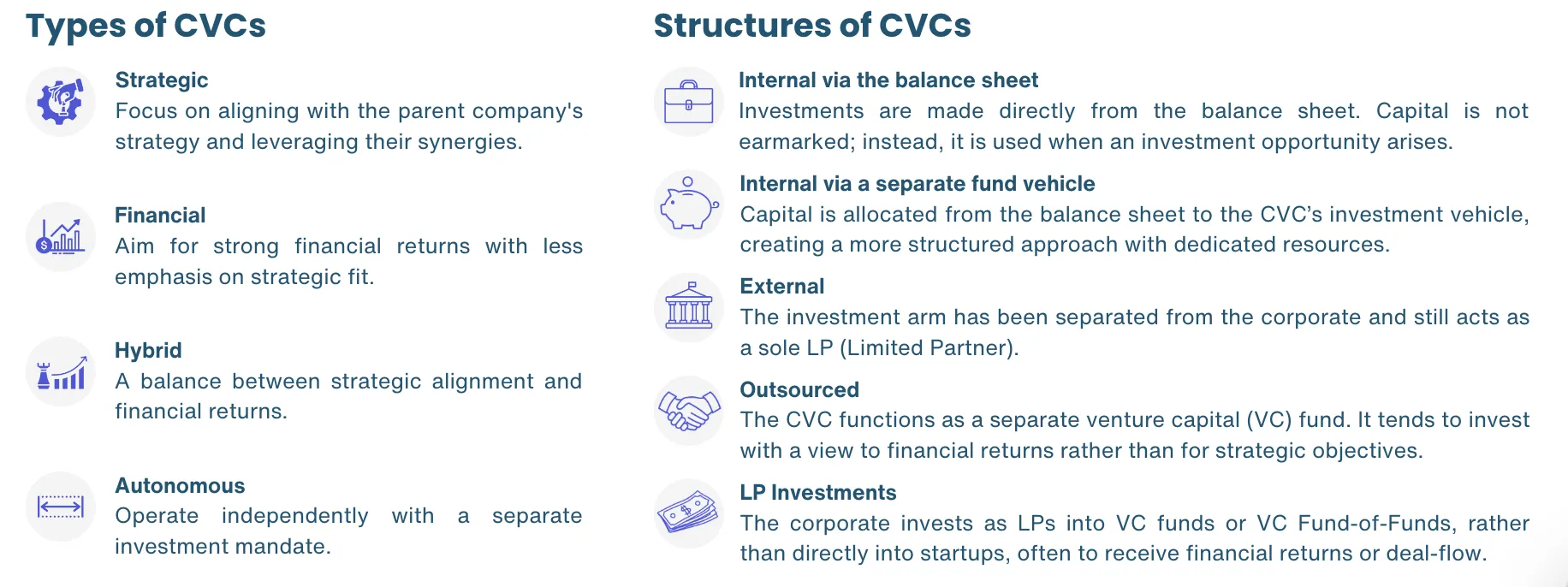

- A Corporate Venture Capital (CVC) fund is an investment vehicle related to a large corporation that invests in startups or funds. These funds can be strategic, financial, hybrid, or autonomous. Their structure varies; they can be organised internally via their balance sheet, internally via a separate vehicle, externally via a subsidiary, fully outsourced, or via LP investments.

- There has been a notable increase in CVCs participating in deals, from 1 in 10 in 2010 to 1 in 4 in 2024, driven by the maturity of the market and the increased appetite from corporates to innovate.

- Founders should consider raising from a CVC for market validation, building a strategic partner, accessing resources, and identifying exit opportunities. However, they should be aware of interest misalignment, a longer investment timeframe, culture incompatibility and be mindful of the terms requested by CVCs.

- For CVCs, investing in startups can provide a competitive edge, improve culture, provide market insights and generate returns.

- This report provides insights from 100+ global CVC investors with over £20 billion in assets under management being deployed into over 600 startups & VCs per year. The majority of CVCs surveyed have a hybrid structure investing internally via their balance sheet.

- A CVC’s appetite to invest in startups is driven by, first and foremost, alignment with the investment thesis, followed by the alignment with their parent company’s business focus, returns, traction and market intelligence. Market intelligence and financial returns are the most important criteria when selecting funds to invest in. In return, internal business opportunities is the most important value-add to founders.

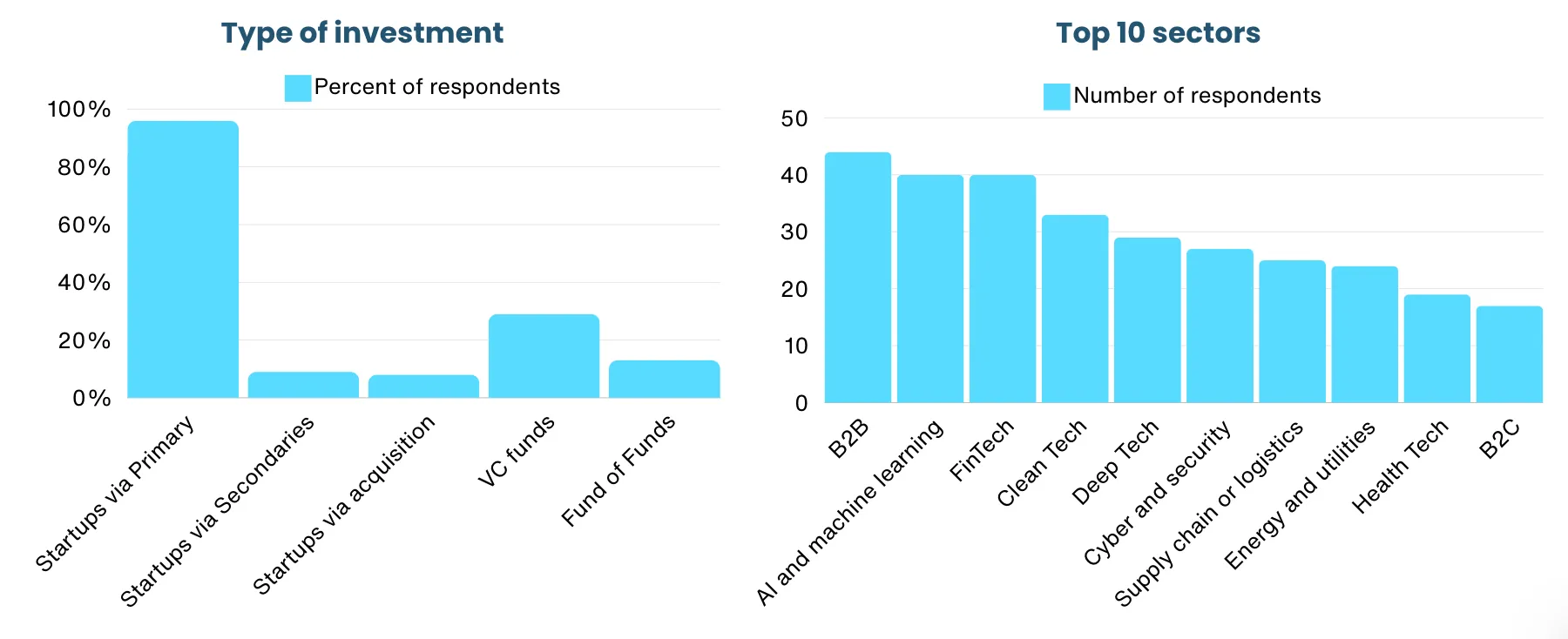

- CVCs are continuing to invest in tech, with the majority (90%) investing the same amount or more in early-stage companies over the next three years. Investing directly into startups was the most common type of investment (95%), Series A (90%) the most common stage and B2B & AI the most common sectors (c. 40%).

- 1 in 3 CVCs invest in VCs or VC FoFs, most prefer specialist over agnostic funds and half are interested in emerging managers.

- Challenges include management buy-in, slow processes & management changes.

What is a Corporate Venture Capital fund and how are they structured?

Corporate venture capital (CVC) is a subset of venture capital (VC), whereby funding comes from corporates, often with a strategic motive.

Advice for founders when raising CVC money

This report explores the world of CVCs both from a founder and corporate perspective. First, we look at advice for founders looking to raise from corporate investors.

Perks for founders of raising from a CVC?

- Market Validation — Securing investment from established corporations can create instant credibility, attracting new business opportunities and further investment from other sources.

- A Long-Term Partnership — Unlike traditional VC firms, CVCs typically embrace a more patient and strategic approach that is focussed on mutual benefit, allowing startups to focus on building a sustainable business above chasing short-term growth opportunities.

- Access to Strategic Resources — CVCs can provide domain expertise and resources, helping to accelerate startups’ product development, market expansion, and overall business scalability.

- Exit Opportunities — CVCs can leverage their corporate network to provide introductions to key industry players. This access to potential acquirers or strategic partners improves the visibility of the startup and lays the groundwork for a future exit or merger.

What should founders be cautious about when raising CVC money

- Loss of Control — Giving away too much equity, accepting consent rights or overreliance on the corporate for business opportunities can lead to a loss of influence over the startup’s strategic direction.

- Misalignment of Priorities — Corporate investors may prioritise alignment with their corporate strategy and block diverging opportunities, such as acquisition offers or financing rounds.

- Longer timeframe to investment — CVCs often move slower than VC funds due to longer decision-making processes and controls designed for larger organisations.

- Cultural Incompatibility — A corporation’s structured, hierarchical, and risk-averse nature can clash with and frustrate an innovative, agile, and risk-taking startup.

- Risk of Idea Appropriation — Given a corporation’s resources and capabilities, it has the ability to replicate innovative ideas. Be cautious of this and protect your IP!

Typical terms requested by CVCs

Founders should be aware that corporate investors may have additional minority protections because of the nature of their investment thesis. Here are a few areas you should watch for and understand:

- Call Options: Call options are more common where CVCs take stakes, often at a predetermined price.

- Control and Consent: Additional rights over an exit and extensive control over compliance issues (often aligning with the corporate’s anti-bribery, CSR and ethics policies).

- Competitor Restrictions: Limits on disclosure of information, the provision of services to, or transfers of equity to competitors.

- Investor Director and Observer Rights: There is a conflict when CVCs take Investment Director rights — most rely solely on observer rights; able to attend and speak at board meetings, but not vote.

- Put Options: Put options are also more common. When triggered (e.g. failing to achieve milestones, regulatory or reputational changes), CVCs have the flexibility to sell their shares back to the company or other exiting shareholders.

- Rights of First Offer: The right to be offered the shares before any external solicitation takes place; if refused, the selling shareholder may solicit third-party offers on the same terms.

- Rights of First Refusal: The rights to be offered any shares being sold by other shareholders in the investee company after the selling shareholder has solicited an offer for their shares from a third party. ROFR to acquire your company can limit your options down the road and be off-putting for other potential acquirers.

Advice for corporates

Second, we look at advice to corporates for setting up a corporate venturing arm.

Benefits

- Competitive Advantage — Supporting startups allows corporates to access the latest technologies and market trends, maintaining their industry leadership. Relationships with entrepreneurs can also aid in future hiring and leadership development.

- Shift and Improve Culture — By investing in and acquiring businesses, traditional corporations can infuse innovative, dynamic and agile “Silicon Valley” style culture into their, often stagnant, DNA.

- Market Insights and Opportunities — Startups provide insights into market trends and customer needs, informing strategic planning and driving growth through R&D, business development, and M&A.

- Financial Returns — Venture capital, being high-risk and high-reward, offers substantial returns that can be reinvested into the corporation, boosting profitability and financial health.

“Make sure top management clearly understands the strategic rationale. Different perceptions and misalignment of objectives can create problems.” Bruno Moraes, Wayra

Challenges

- Cultural Misalignment — Startups have very different cultures compared to large corporations and so, post-investment, may struggle to integrate their innovative but often chaotic nature into a more structured environment. This can lead to misunderstandings, misaligned expectations and friction.

- Financial Risk — Investing in startups is inherently risky. High failure rates in the startup ecosystem can lead to significant financial losses, which can negatively impact the corporation’s financial health.

- Divergence from Core Strategic Focus — Allocating resources to support startup investments may cause the corporation to spread itself too thin. This distraction may lead to underperformance and misalignment with its primary business activities and long-term goals.

- Reputational Risk — Investing in a startup will align it with the corporation’s brand. If, however, the startup then encounters ethical issues or controversy, it can reflect poorly on the corporate investor, thereby damaging its own brand and reputation.

What does the data say?

There has been a notable increase in CVCs participating in deals, from 1 in 10 in 2010 to 1 in 4 in 2024, driven by the maturity of the market and the increased appetite from corporates to innovate.

Results of the report

Investment Appetite

The majority of Corporates invest into startups with 1 in 3 also investing in VC funds or VC Fund-of-Funds.

Investment Focus

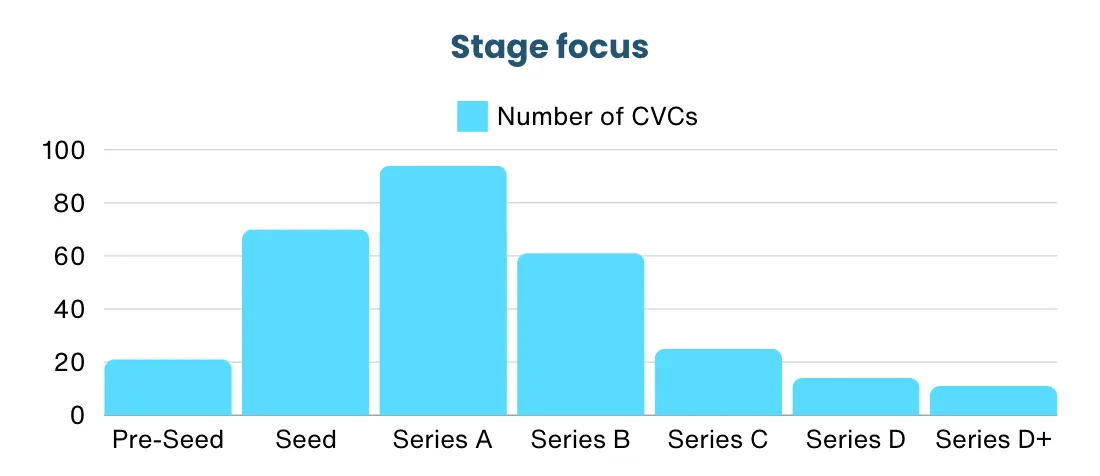

90% of CVCs invest at the Series A stage.

Strategic alignment

In addition to the founder benefits listed above in the qualitative part of the report, CVCs identify the following value-add as significant to the founders they back:

- Internal business opportunities

- Access to enterprise customers

- Access to the executive team

- Product development

- Data exchanges

CVCs as Limited Partners

1 in 3 CVCs invest in VCs or VC FoFs, most prefer specialist over agnostic funds. When raising from LPs, VCs should, as a result, include Corporates as part of their strategy.

Market intelligence and financial returns are the most important criteria when selecting funds to invest in.

Over half are interested in investing in Emerging Managers and around half had already invested in them, due to their sector expertise, operational track record and differentiated strategy.

Opportunities for the CVC ecosystem

Constraints on VC deployment create opportunities for CVC investors who are not restricted by fund timelines/deadlines

“As a CVC with no need to raise capital and with the flexibility to deploy as needed, we stand apart.”

Founders are increasingly drawn towards CVCs because they value investors who can demonstrate sector knowledge, networks and tangible support

“The opportunity to transform the core business through investments and networks developed with startups allows us to leapfrog competition.”

“CVCs provide strategic value to the startups, helping them to dive into a specific industry and access PoCs“

Challenges for the CVC ecosystem:

“CVCs are usually too strategic and not enough financially driven”

“Management changes can result in volatile support for a CVC, making them unreliable sources of capital.”

“CVCs with a strategic angle are too slow from a process standpoint to get into hot deals.

“Long deployment times and poor incentive alignment”

Diversity and Inclusion

CVCs, like the rest of Venture Capital, have a long way to go to reach proportionate representation. We hope to encourage more progress by sharing some stats about the current state of diversity within the CVC ecosystem.

- 3 in 8 CVCs FoFs have a focus towards diversity investing, with women being the most sought groups after due to positive change in the ecosystem, better returns and better governance.

- 10% identified as intersectional and 3% identified as LGBTQ+

- White was the most common ethnic background, representing 77% of the respondents. Other respondents indicated they were Mixed Race, East Asian, Black and Other.

- There was a diverse spread of countries participants were born in and a diverse spread of educational backgrounds.

Deep dive interviews

We interviewed two active CVCs in Europe and reproduced the Q&A in the report. View the full report below to see what they invest in, what they think of the landscape and their corporate and founder tips.

Download the full report

👉 For a deeper dive and to explore the full analysis which includes more information on what CVCs are investing in, and additional insights for VCs, the report is accessible free to download here.