June 04, 2026

By

From Crisis to Opportunity: Venture's Role in UK Housing

The venture case for backing Britain's housing crisis

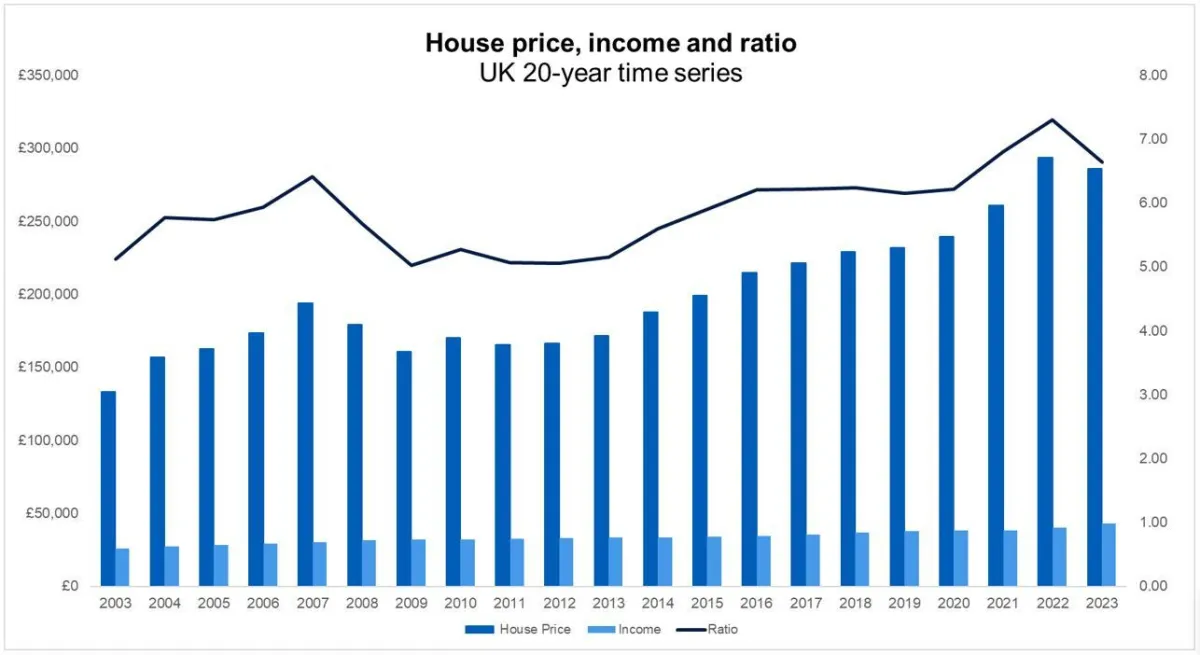

There is no doubt that we are in the middle of a housing crisis in this country. Not just due to the lack of homes being built but also the sheer cost of them. The average house price in London is c.£500k which represents a price to income ratio of 12x. Even when we look outside of London, housing can hardly be considered affordable with all regions in the UK sitting above 6x.

Encouraging housing development and making it easier to get on the housing ladder are regularly shown to be two of the most important things for younger voters, but what does this look like in practice and how, if at all, can venture help?

Halifax: House prices, income and ration

Current State of Play

In 1968 Great Britain built 425,000 homes in a single year. Throughout the post-war period the average was well above 300,000. Despite this being the target for numerous governments in the last 30 years, that average has not been reached since. In fact, in 2025 170,000 homes were built which represents a c.8% drop on 2024.

The collapse was gradual. It began in the 1970s as council housebuilding wound down, especially following the 1980 Right to Buy scheme, private developers never filled the gap. The planning system, land costs, skills shortages in construction, and viability constraints on developers have all kept output persistently low relative to need.

Growth in London house prices is now more reflective of global wealth than UK wealth. Since the rest of the world is outstripping the UK in rates of growth (back to that productivity issue again), UK citizens will continue to see their relative purchasing power erode.

Public and Private Partnerships

The last few years have shown the state is either unable or unwilling to meet not only its own housing targets but also the housing needs of the public. The government doesn't have the engineering capacity, the operating model or the political appetite to fix this on its own. That leaves ample room for founders to capitalise on the malaise and shake things up.

We've been looking at this space at Love Ventures for over five years and have backed companies on both sides of the equation: the supply side (getting more homes built) and the demand side (helping people access them). What's been encouraging over that period is the pace at which UK founders have built credible businesses in areas that previously had none. There is now a startup having a serious crack at almost every node in the system.

Fixing the supply side

Supply is broken at almost every stage of the process: land sourcing, planning, surveys, materials and labour. Each one is its own bottleneck, and the cumulative drag of them is what has held UK output below 200,000 homes a year despite decades of political promises to do better.

Land: Identifying viable development sites is still one of the most manual parts of the chain. The big housebuilders rely on incumbent processes and patchy data. Overlaying planning constraints, environmental designations, infrastructure and ownership is largely manual and inconsistently done. AI is starting to collapse weeks of analyst work into minutes and surface plots that the market has historically overlooked.

Planning: The UK planning system is the single biggest structural drag on housebuilding. Councils are under-resourced, planners are leaving for the private sector, backlogs are growing, and most departments are still running software built in the 1990s. There is a new wave of startups building AI tooling for local authority planning officers that automates application processing, document extraction and officer workflows. The point isn't to replace planners, it's to free up scarce human capacity to focus on the difficult decisions rather than the administrative slog. This is the kind of public-private collaboration the problem demands: private teams building the digital infrastructure the public sector has not been able to build itself.

Surveys: Before a brick is laid, developers need asbestos, ecology, contamination and utilities reports. Procurement of these is fragmented and slow, and often adds weeks to project timelines for work that is largely standardised. Marketplaces that compress the loop to minutes and plug directly into the Planning Portal are quietly removing a real source of delay.

Construction: Construction is the second least digitised sector in the economy, after agriculture. Contractor margins sit at 2-6%, merchants take 30-40%, materials are still procured over WhatsApp, and design changes are propagated manually across a dozen software platforms that don't talk to each other. The opportunity is significant and unglamorous: digitise procurement to strip out middleman margin, and automate design change propagation to claw back the productivity currently being lost to admin.

Modular: Modular has been "about to transform housing" for thirty years and has repeatedly failed because the factories were too big, too capital intensive and too far from the sites they were serving. The newer thesis, distributed robotic micro-factories producing timber components locally, looks more promising, and crucially it's a model that local authorities and registered providers can plug into directly.

Ones to watch on the supply side: Tract (land), Xylo (planning), Renkap (surveys), Prolo and Byte Engineering (construction), AUAR (modular).

Fixing the demand side

The other half of the equation is access. Even when homes do exist, the system that decides who gets them is brutally exclusionary, and this is where public policy and private innovation are colliding most obviously.

Renting: Several million UK renters struggle with the referencing process: foreign income, self-employment, thin credit files, or simply being young. Until recently, landlords worked around it by accepting six to twelve months' rent upfront. The Renters Rights Act, in force from May 2026, has ended that practice and made a guarantor effectively mandatory. The UK guarantor market was not built for this volume, and a wave of digital guarantor providers is now moving in to fill the gap: same-day decisions, insurance-backed, materially cheaper than the incumbents. The bigger prize sits underneath. Rent is the largest and most consistent financial commitment most people ever make, and it has counted for almost nothing in credit decisions. Turning rental payment history into usable financial data unlocks mortgages, credit and savings products for a generation that has been locked out of all three.

Buying: The affordability gap between renting and owning is the defining financial problem for under-40s in the UK. High street lenders don't package the products that actually help (guarantor mortgages, family deposit boosters, shared equity) coherently or accessibly, and the traditional 95% LTV mortgage is increasingly insufficient given the multiples involved. A new generation of brokers and lenders is rebuilding that layer specifically for first time buyers. Gradual homeownership models, where people buy a share of a home and increase their stake over time, are also starting to attract serious institutional capital and offer a credible stepping stone for the millions priced out of the traditional mortgage market. One of the start ups tackling this specific issue is Tembo, whom Love Ventures have previously backed, looking to make it easier for young people to save and get on the housing ladder.

Build-to-Rent: Institutional capital is finally flowing into UK rental at scale and BTR is now a meaningful share of new urban supply. Whether that translates into a better product than the cottage industry landlord market it is replacing depends almost entirely on the operating layer: the software that handles leasing, tenant experience, maintenance and turnover. The startups building this layer are the ones doing the work to turn institutional capital into housing that residents actually want to live in.

Ones to watch on the demand side: Rentmigo (renting), Tembo and Wayhome (buying), Residently (BTR).

The common thread across all of these is that regulation has been a help rather than a hindrance. The Renters Rights Act didn't kill the rental market, it created an entirely new category of digital guarantor. Net zero targets, EPC requirements and the planning backlog are creating the pull for the planning, surveying and retrofit wave behind them. The best housing founders aren't fighting the public sector, they're partnering with it and getting on with the work that the government has not been able to deliver itself.

Our Request to You

To founders, if you are operating in the property sector please do get in touch. Before expanding our thesis to Future of Work, Proptech was one of our first investment pillars and a good number of our 260 investors are in the property industry so we have a deep well of expertise upon which you can call.

To investors, as funds we of course want to make our LP’s money but it is important to remember that we do so in the context of a nation that is facing challenges from all sides. High tax, broken infrastructure, and a housing market that is on it’s knees. If we as fund managers can make a small bit of difference, then that is something we should grab with both hands.

Photo by Mark Stuckey on Unsplash